Mortgage Credit Availability Index

Complimentary for MBA Members! The Mortgage Credit Availability Index (MCAI) is a barometer on the availability or supply of mortgage credit at a point in time, using criteria from institutional investors who purchase loans through the broker and/or correspondent channels. The MCAI is calculated using several factors related to borrower eligibility (credit score, loan type, loan-to-value ratio, etc.) using data made available by ICE Mortgage Technology. These metrics and the underwriting criteria for numerous lenders/investors are analyzed and, through a proprietary formula, MBA calculates the MCAI which include indices for Total, Conventional, Government, Conforming and Jumbo segments. The base period and values for the total index is March 31, 2012=100; Conventional March 31, 2012=73.5; Government March 31, 2012=183.5.

Questions about MBA Research? Contact the MBA Research team.

Questions about ICE Mortgage Technology? Visit their website.

Related Press Releases

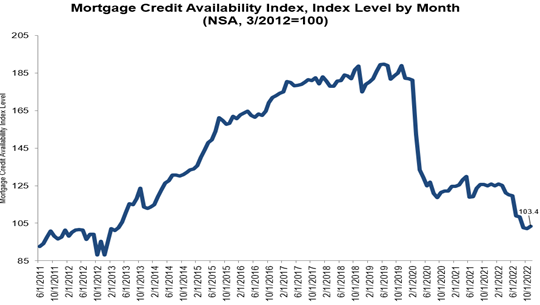

Mortgage Credit Availability Increased in November

Mortgage credit availability increased in November according to the Mortgage Credit Availability Index (MCAI), a report from the Mortgage Bankers Association (MBA) that analyzes data from ICE Mortgage Technology.

The MCAI rose by 1.4 percent to 103.4 in November. A decline in the MCAI indicates that lending standards are tightening, while increases in the index are indicative of loosening credit. The index was benchmarked to 100 in March 2012. The Conventional MCAI increased 2.8 percent, while the Government MCAI remained unchanged. Of the component indices of the Conventional MCAI, the Jumbo MCAI increased by 3.9 percent, and the Conforming MCAI rose by 1.0 percent.

“Credit availability increased slightly in November, the first increase in nine months as lenders continued to navigate a challenging environment brought on by higher rates and a much slower housing market,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Jumbo credit availability saw a 4 percent increase, as jumbo rates remained more competitive than rates on conforming loans. Lenders are seeking to capture more volume in this space. Most of last month’s increase came from more ARM loan programs being offered.”

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

CONVENTIONAL, GOVERNMENT, CONFORMING, AND JUMBO MCAI COMPONENT INDICES

The MCAI rose by 1.4 percent to 103.4 in November. The Conventional MCAI increased 2.8 percent, while the Government MCAI remained unchanged. Of the component indices of the Conventional MCAI, the Jumbo MCAI increased by 3.9 percent, and the Conforming MCAI rose by 1.0 percent.

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

The Conventional, Government, Conforming, and Jumbo MCAIs are constructed using the same methodology as the Total MCAI and are designed to show relative credit risk/availability for their respective index. The primary difference between the total MCAI and the Component Indices are the population of loan programs which they examine. The Government MCAI examines FHA/VA/USDA loan programs, while the Conventional MCAI examines non-government loan programs. The Jumbo and Conforming MCAIs are a subset of the conventional MCAI and do not include FHA, VA, or USDA loan offerings. The Jumbo MCAI examines conventional programs outside conforming loan limits, while the Conforming MCAI examines conventional loan programs that fall under conforming loan limits.

The Conforming and Jumbo indices have the same “base levels” as the Total MCAI (March 2012=100), while the Conventional and Government indices have adjusted “base levels” in March 2012. MBA calibrated the Conventional and Government indices to better represent where each index might fall in March 2012 (the “base period”) relative to the Total=100 benchmark.

EXPANDED HISTORICAL SERIES

The Total MCAI has an expanded historical series that gives perspective on credit availability going back approximately 10-years (expanded historical series does not include Conventional, Government, Conforming, or Jumbo MCAI). The expanded historical series covers 2004 through 2010, and was created to provide historical context to the current series by showing how credit availability has changed over the last 10 years – including the housing crisis and ensuing recession. Data prior to March 31, 2011, was generated using less frequent and less complete data measured at 6-month intervals and interpolated in the months between for charting purposes. Methodology on the expanded historical series from 2004 to 2010 has not been updated.

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

Data prior to 3/31/2011 was generated using less frequent and less complete data measured at 6-month intervals interpolated in the months between for charting purposes.

ABOUT THE MORTGAGE CREDIT AVAILABILITY INDEX

The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit.

The MCAI is calculated using several factors related to borrower eligibility (credit score, loan type, loan-to-value ratio, etc.). These metrics and underwriting criteria for over 95 lenders/investors are combined by MBA using data made available via ICE Mortgage Technology and a proprietary formula derived by MBA to calculate the MCAI, a summary measure which indicates the availability of mortgage credit at a point in time. Base period and values for total index is March 31, 2012=100; Conventional March 31, 2012=73.5; Government March 31, 2012=183.5.

To learn more about the ICE Mortgage Technology platform click here.

For more information on the Mortgage Credit Availability Index, including Methodology, Frequently Asked Questions and other helpful resources, please contact [email protected].

Leave a comment