Chart of the Week: Property Type Mix Varies by Capital Source

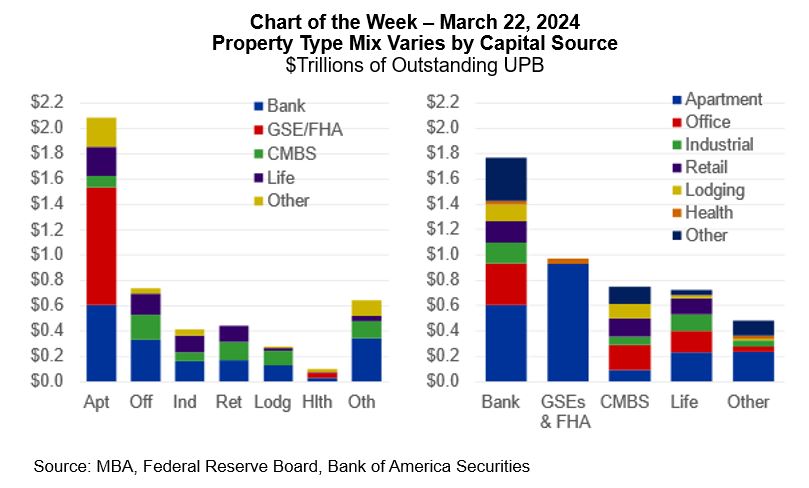

This week’s Chart of the Week (COTW) shows MBA’s estimates of the distribution of CRE mortgage debt across capital sources and property types and is derived from a variety of public and private sources. As can be seen, CRE mortgage debt is not a monolithic market. Rather, it is made up of a broad range of intersections—across property types and capital sources (shown above), as well as property subtypes, metro markets and submarkets, owner types, vintages, and more.

Commercial banks continue to hold the largest share (38 percent) of the $4.7 trillion of commercial mortgage debt outstanding at $1.8 trillion, but the bank total is split between apartments (roughly 34 percent of the bank total), office (19 percent), retail (9 percent), industrial (9 percent), and a range of other property types, including lodging, health care, self-storage, data centers, and more. Agency and GSE portfolios and MBS are the second largest holders of commercial mortgage debt at $1.0 trillion (21 percent of the total). Life insurance companies hold $733 billion (16 percent) and CMBS, CDO. and other ABS issues hold $593 billion (13 percent).

Careful observers may notice that MBA’s $4.7 trillion figure for CRE mortgage debt outstanding differs from a figure some other sources cite, a number closer to $5.8 trillion. The key difference is that MBA purposefully excludes some types of loans that the other figure includes—most impactfully loans backed by owner-occupied properties and estimates of construction loans outstanding.

When speaking with our members and others in the commercial real estate space, it is clear that loans backed by owner-occupied properties aren’t really “CRE mortgages.” Unlike income-producing properties, they don’t have leases, rents, vacancy rates, net operating incomes, capitalization rates, or any of the other key characteristics that make CRE lending what it is. Rather, loans collateralized by owner-occupied properties are more generally underwritten and approached by lenders as commercial and industrial loans to which the property is pledged in “an abundance of caution.” Of note, the regulators’ proposed changes to capital risk weights as part of the Basel III endgame, along with many other elements of their guidance, follow the same general approach as MBA.

The CRE debt markets are getting a great deal of attention at present. When one knows where to look, there is plenty of information to help one understand what’s happening where. Like the market itself, however, that data tends not to come in one big block but is rather in pockets covering specific component pieces.