Mortgage Delinquencies Increase in the Fourth Quarter of 2022

February 16, 2023

Share to

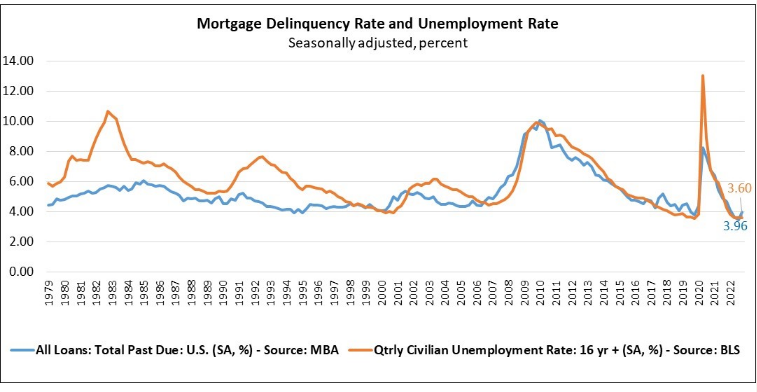

WASHINGTON, D.C. (February 16, 2023) – The delinquency rate for mortgage loans on one-to-four-unit residential properties increased to a seasonally adjusted rate of 3.96 percent of all loans outstanding at the end of the fourth quarter of 2022, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

The delinquency rate was up 51 basis points from the third quarter of 2022 but still down 69 basis points from one year ago. The percentage of loans on which foreclosure actions were started in the fourth quarter fell by 1 basis point to 0.14 percent.

“As expected, the overall national mortgage delinquency rate increased in the fourth quarter of 2022 from its previous quarterly survey low,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “The weaker economy and ongoing inflationary pressures contributed to the uptick in delinquencies. The delinquency rate – while still low – increased from the previous quarter across all loan types and across all stages of delinquency.”

According to Walsh, for the past 15 years, mortgage delinquencies have tracked very closely with employment conditions. Despite recent indicators of resiliency in the job market, including the unemployment rate declining to 3.4 percent in January, MBA still forecasts for slower hiring and rising unemployment, with the rate rising to 5.2 percent by the end of the year. This will likely mean further increases in mortgage delinquencies.

Added Walsh, “Notwithstanding the fourth-quarter increase in mortgage delinquencies, the foreclosure starts rate of 0.14 percent was well below the historical quarterly average of 0.40 percent. Many distressed homeowners have loss mitigation options available to them and have accumulated home equity, which can ease financial hardship and avert foreclosure actions.”

Key findings of MBA's Fourth Quarter of 2022 National Delinquency Survey:

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

- Compared to last quarter, the seasonally adjusted mortgage delinquency rate increased for all loans outstanding. By stage, the 30-day delinquency rate increased 26 basis points to 1.92 percent, the 60-day delinquency rate increased 13 basis points to 0.66 percent, and the 90-day delinquency bucket increased 11 basis points to 1.38 percent.

- By loan type, the total delinquency rate for conventional loans increased 26 basis points to 2.78 percent over the previous quarter. The FHA delinquency rate increased 209 basis points to 10.61 percent, and the VA delinquency rate increased by 45 basis points to 4.16 percent.

- On a year-over-year basis, total mortgage delinquencies decreased for all loans outstanding. The delinquency rate decreased by 80 basis points for conventional loans, decreased 15 basis points for FHA loans, and decreased 108 basis points for VA loans from the previous year.

- The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the fourth quarter was 0.57 percent, up 1 basis point from the third quarter of 2022 and 15 basis points higher than one year ago.

- The non-seasonally adjusted seriously delinquent rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 1.89 percent. It decreased by 1 basis point from last quarter and decreased by 94 basis points from last year. The seriously delinquent rate decreased 5 basis points for conventional loans, increased 14 basis points for FHA loans, and decreased 8 basis points for VA loans from the previous quarter. Compared to a year ago, the seriously delinquent rate decreased by 68 basis points for conventional loans, decreased 208 basis points for FHA loans and decreased 139 basis points for VA loans.

- The five states with the largest quarterly increases in their overall delinquency rate were: Louisiana (77 basis points), Florida (74 basis points), Indiana (62 basis points), West Virginia (55 basis points), and Mississippi (55 basis points).

- Note: For the purposes of the survey, MBA asks servicers to report loans in forbearance as delinquent if the payment was not made based on the original terms of the mortgage.