IMBs Report Net Production Losses in the First Quarter of 2024

May 23, 2024

Share to

WASHINGTON, D.C. (May 23, 2024) — Independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks reported a pre-tax net loss of $645 on each loan they originated in the first quarter of 2024, a decrease from the reported loss of $2,109 per loan in the fourth quarter of 2023, according to the Mortgage Bankers Association’s (MBA) newly released Quarterly Mortgage Bankers Performance Report.

“While the first quarter of 2024 marks the eighth consecutive quarter of net production losses, these losses were less severe than the previous two quarters,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “In basis points, production revenue rose above the historical average and production costs declined. This led to an improvement in the production bottom line by almost 50 basis points during the quarter.”

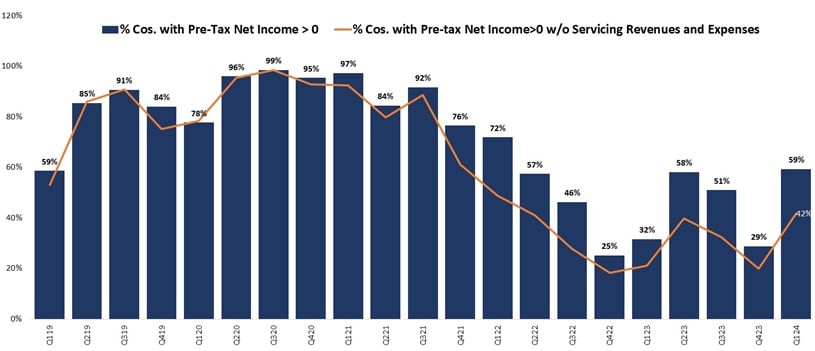

Noted Walsh, “Servicing profitability also improved, given low prepayment activity and preservation of servicing values. Including both the production and servicing business lines, close to 60 percent of mortgage companies were profitable in the first quarter of this year – the highest level in eight quarters.”

Key findings of MBA’s First-Quarter 2024 Quarterly Mortgage Bankers Performance Report include:

- Including all business lines (both production and servicing), 59 percent of the firms in the report posted pre-tax net financial profits in the first quarter of 2024, up from 29 percent in the fourth quarter of 2023.

- The average pre-tax production loss was 25 basis points (bps) in the first quarter of 2024, compared to an average net production loss of 73 bps in the fourth quarter of 2023, and a loss of 68 basis points one year ago. The average quarterly pre-tax production profit, from the third quarter of 2008 to the most recent quarter, is 42 basis points.

- The average production volume was $384 million per company in the first quarter, up from $359 million per company in the fourth quarter. The volume by count per company averaged 1,193 loans in the first quarter, up from 1,170 loans in the fourth quarter.

- Total production revenue (fee income, net secondary marketing income and warehouse spread) increased to 371 bps in the first quarter, up from 334 bps in the fourth quarter. Average quarterly production revenue, from the third quarter of 2008 to the most recent quarter, is 347 basis points. On a per-loan basis, production revenues increased to $11,947 per loan in the first quarter, up from $10,376 per loan in the fourth quarter.

- The purchase share of total originations, by dollar volume, was 85 percent. For the mortgage industry as a whole, MBA estimates the purchase share was at 77 percent in the first quarter of 2024.

- The average loan balance for first mortgages increased to $345,761 in the first quarter, up from $336,757 in the fourth quarter.

- Total loan production expenses – commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations – decreased to 395 basis points in the first quarter of 2024 from 407 basis points in the fourth quarter of 2023. However, per-loan costs increased to $12,593 per loan in the first quarter, up from $12,485 per loan in the fourth quarter of 2023. From the first quarter of 2008 to last quarter, loan production expenses have averaged $7,472 per loan.

- Median productivity – measured as loans closed per retail / consumer direct production employee – remained unchanged at 1.1 loans per employee in the first quarter.

- Servicing net financial income for the first quarter (without annualizing) was $82 per loan, up from a negative $24 per loan in the fourth quarter. Servicing operating income, which excludes MSR amortization, gains/loss in the valuation of servicing rights net of hedging gains/losses, and gains/losses on the bulk sale of MSRs, was $93 per loan in the first quarter, down from $108 per loan in the fourth quarter.

MBA's Mortgage Bankers Performance Report series offers a variety of other performance measures on the mortgage banking industry including revenue and cost breakouts, productivity, product mixes for originations and servicing volume, and pull-through rates. MBA's Mortgage Bankers Performance Report is intended as a financial and operational benchmark for independent mortgage companies, bank subsidiaries and other non-depository institutions. Eighty-four percent of the 338 companies that reported production data for the first quarter of 2024 were independent mortgage companies, and the remaining 16 percent were subsidiaries and other non-depository institutions.

There are five Mortgage Bankers Performance Report publications per year: four quarterly reports and one annual report. Media wishing to view a copy of either report should contact Falen Taylor at (202) 557-2771 or [email protected]. To purchase or subscribe to the publications, call (202) 557-2879. The reports can also be purchased on MBA's website by visiting www.mba.org/PerformanceReport.