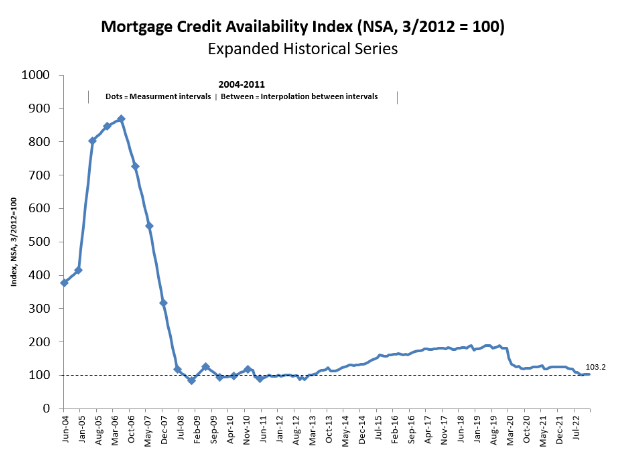

Mortgage Credit Availability Index

Complimentary for MBA Members! The Mortgage Credit Availability Index (MCAI) is a barometer on the availability or supply of mortgage credit at a point in time, using criteria from institutional investors who purchase loans through the broker and/or correspondent channels. The MCAI is calculated using several factors related to borrower eligibility (credit score, loan type, loan-to-value ratio, etc.) using data made available by ICE Mortgage Technology. These metrics and the underwriting criteria for numerous lenders/investors are analyzed and, through a proprietary formula, MBA calculates the MCAI which include indices for Total, Conventional, Government, Conforming and Jumbo segments. The base period and values for the total index is March 31, 2012=100; Conventional March 31, 2012=73.5; Government March 31, 2012=183.5.

Questions about MBA Research? Contact the MBA Research team.

Questions about ICE Mortgage Technology? Visit their website.

Related Press Releases

Mortgage Credit Availability Remained Flat in January

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

CONVENTIONAL, GOVERNMENT, CONFORMING, AND JUMBO MCAI COMPONENT INDICES

The MCAI fell by 0.1 percent to 103.2 in January. The Conventional MCAI decreased 0.3 percent, while the Government MCAI remained unchanged. Of the component indices of the Conventional MCAI, the Jumbo MCAI decreased by 0.4 percent, and the Conforming MCAI remained unchanged.

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

Source: Mortgage Bankers Association; Powered by ICE Mortgage Technology

Data prior to 3/31/2011 was generated using less frequent and less complete data measured at 6-month intervals interpolated in the months between for charting purposes.

ABOUT THE MORTGAGE CREDIT AVAILABILITY INDEX

The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit.

The MCAI is calculated using several factors related to borrower eligibility (credit score, loan type, loan-to-value ratio, etc.). These metrics and underwriting criteria for over 95 lenders/investors are combined by MBA using data made available via ICE Mortgage Technology and a proprietary formula derived by MBA to calculate the MCAI, a summary measure which indicates the availability of mortgage credit at a point in time. Base period and values for total index is March 31, 2012=100; Conventional March 31, 2012=73.5; Government March 31, 2012=183.5.

To learn more about the ICE Mortgage Technology platform click here.

For more information on the Mortgage Credit Availability Index, including Methodology, Frequently Asked Questions and other helpful resources, please contact [email protected].

Leave a comment